Sejal Glass Limited.

Sejal Glass: A Silent Leader Rising in the Glass Industry

So, today we are talking about a new company.

A company which has caught my eye, but let me be very clear from the beginning — this is a non-liquid stock.

Now, what do I mean by non-liquid?

A non-liquid stock is a stock where trading volume is very low. Very few shares are traded daily, and sometimes you may even find it difficult to buy or sell shares at your desired price.

In this company, the average daily traded value is only around ₹2 to ₹2.5 crore, which is extremely low compared to mid and large caps.

So yes, this stock will be volatile, it can move sharply up or down.

But many times, the best stories are hidden in such non-liquid names.

And the company we are discussing today is Sejal Glass Limited.

What Does Sejal Glass Do?

Sejal Glass does nothing complicated.

And honestly, that’s exactly why I like it.

I personally prefer investing in simple businesses. Businesses which don’t need rocket science to understand. Because in the long run, simple businesses make the most money.

So what does Sejal Glass do?

Very simple:

They manufacture and process glass.

Their product portfolio includes:

Toughened glass

Laminated glass

Insulated glass (IG units)

Decorative and digitally printed glass

And other value-added architectural glass products

This glass is used in commercial buildings, residential towers, facades, airports, metros, railways, offices, hospitals, and infrastructure projects.

Where Does Sejal Glass Operate?

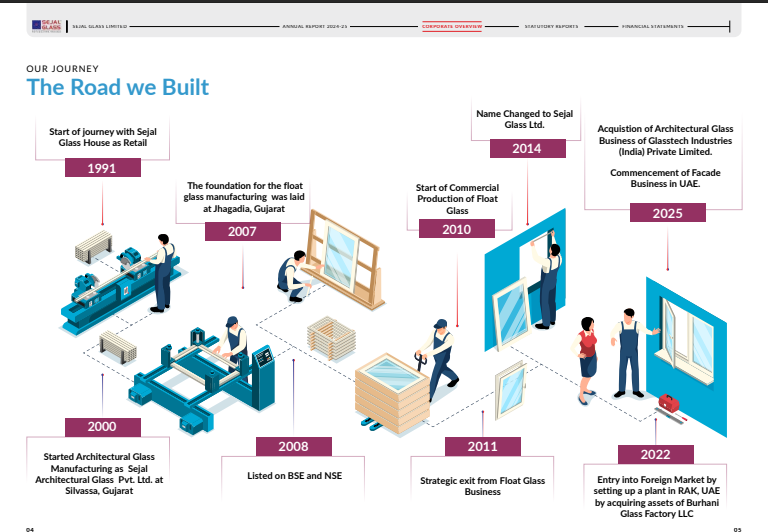

Sejal Glass has a strong manufacturing footprint, both in India and overseas.

🇮🇳 India Operations

They operate through three manufacturing units:

Silvassa

Taloja (near Mumbai)

Erode (near Coimbatore)

This gives them presence across West and South India, which is very important for logistics and project execution.

🇦🇪 International Operations

They also have one manufacturing plant in Ras Al-Khaimah, UAE.

This UAE plant is a big export hub, catering to:

GCC region

Africa

Europe

Exports form a major part of their business, which gives them currency diversification and better realisations.

Who Runs the Show?

The company is promoted by the Gada family, under the Sejal Group, who are long-time players in the glass industry.

Promoter holding is around 69%, which shows strong skin in the game.

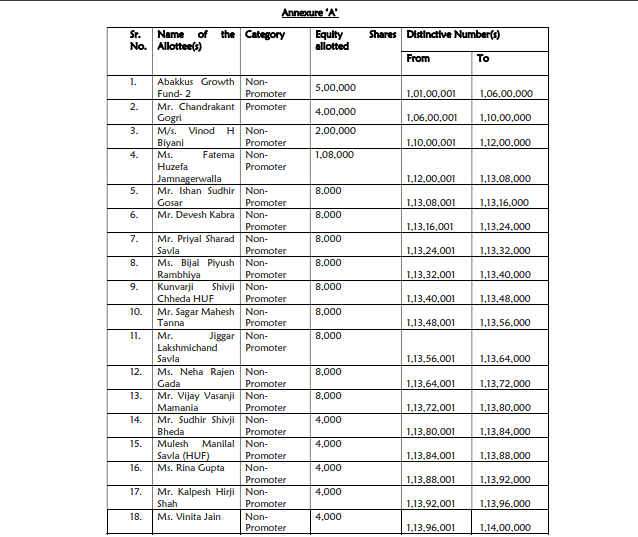

There was also a preferential allotment done at ₹555, where some very strong names came in:

Sunil Singhania via Abakkus Growth Fund

Chandrakant Gogri [Promoter of Aarti Industries Ltd]

Along with several HNIs

This clearly tells you that smart money has done its homework here.

Preferential Allotment

Preferential allotment is when a company raises money from institutions or HNIs by issuing shares directly to them, usually at a discount to the market price.

For example:

Market price = ₹500

Preferential issue price = ₹400–₹450

The risk is that these shares come with a lock-in period.

Investors cannot sell immediately

Lock-in can be 6 months or 1 year, depending on the agreement

So, preferential allotment shows long-term confidence from institutions, but the money is not quick or easy to exit.

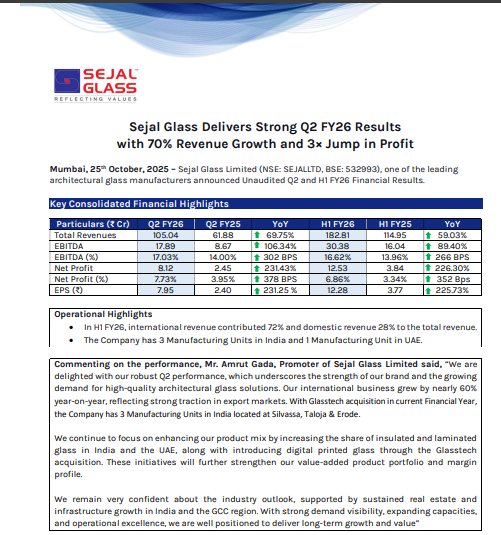

Latest Financial Performance (Q2 & H1 FY26)

Now let’s talk numbers, because numbers tell the real story.

Q2 FY26

Revenue: ₹105 crore

YoY growth: ~70%

PAT: ₹8.1 crore

PAT margin: ~7% to 7.7%

H1 FY26

Revenue growth: ~59% YoY

These are strong numbers, especially for a manufacturing company, and clearly indicate:

Demand momentum

Better product mix

Operating leverage starting to show.

Operating leverage simply means a situation where profits (PAT) grow faster than sales, because fixed costs are spread over higher revenues.

Revenue & Valuation – My Rough Estimates (Not Guidance)

Now let’s talk about revenue estimates, purely from an investor’s point of view.

Management is guiding for ~₹400 crore revenue in FY26. To stay conservative, I’ll assume ₹380–400 crore.

PAT margins are clearly on an improving trend, but to avoid over-optimism, I’ll assume only a 5% PAT margin.

Revenue: ₹380–400 crore

PAT margin (conservative): 5%

Estimated PAT: ₹20–22 crore

At this PAT level, the stock trades at roughly a forward PE of ~40.

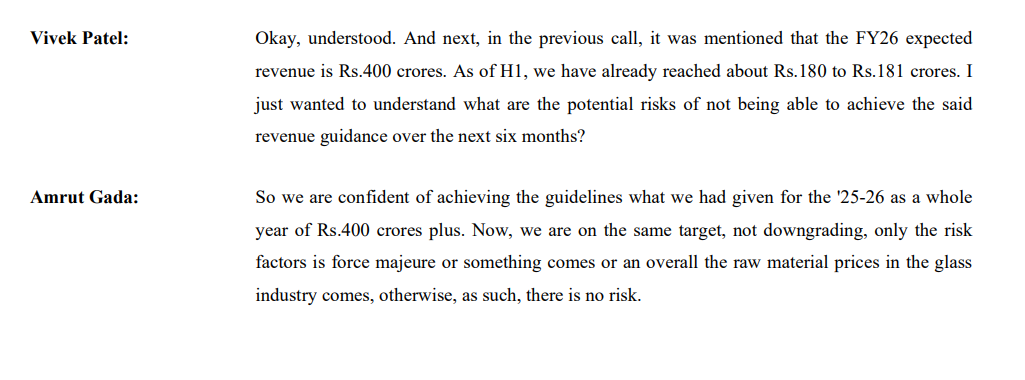

Sejal Glass Q2FY26 Concall

Now here’s the interesting part.

If I’m paying a 40 PE for a company growing sales at ~60%, the PEG ratio comes to ~0.7, which is clearly undervalued by growth standards.

In my view, at current levels, this stock is undervalued and worth watching closely.

If everything goes right — meaning management executes well and delivers on guidance — then in a healthy market, a company like Sejal Glass Limited can easily command a PE of 60.

At that valuation, the intrinsic price can move towards ₹1600–1700 over time.

Important disclaimer:

Revenue guidance is from management

Valuation and target price are my personal rough estimates

Always remember:

EPS is controlled by the company

PE is given by the market and sentiment

If the company operates in the right direction, EPS will grow — and the market decides what multiple to assign.

Key Risks (According to Me)

The main risk for the company is raw material prices.

If glass or input costs rise sharply and the company fails to pass it on, margins can take a hit. Also, any mismanagement at the execution level can create short-term issues.

Apart from this, I don’t see any major structural risk as of now.

If we look at the numbers, the company has already done ~₹170 crore revenue in the first two quarters combined, which gives decent confidence on the FY26 revenue guidance.

So yes, based on current execution and run-rate, achieving the numbers looks very much possible — provided things remain on track.

Technicals & My View

From a pure chart perspective, the stock formed a classic VCP pattern, broke out around September, and rallied nearly 40% from the breakout zone.

However, in the current market correction, the stock is struggling.

That said, this is not a stock to be judged on technicals.

Why?

Because this is a highly illiquid stock.

With an average daily traded value of just ₹2–2.5 crore, candles, patterns, and short-term price action lose their relevance, especially for a company with a market cap of ~₹800 crore.

So instead of focusing on charts, the only thing that matters here is business execution and improvement.

If the company executes well and delivers on what management is guiding, this stock has the potential to be a 2–3x from here over time.

But let me be very clear:

This is a high-risk stock

Liquidity risk is real

Volatility will be high

Overall, I am bullish, but this is a stock that needs to be watched very closely, not blindly chased.

If you’re still here, thank you so much for taking the time to read this — I truly appreciate it.

And always remember, consult your financial advisor before making any investment decisions.

This content is purely for educational purposes and reflects my personal views.