How I Think About the Market & Investing

Lessons I learned from the markets.

How I Think About the Market & Investing

I always look at the future, because the market itself is forward-looking.

The market does not reward what has already happened — it rewards what is expected to happen next.

That’s why I pay close attention to management guidance.

If a company is currently growing at 50% sales growth, I want management to guide for:

50% growth going forward, or

at least 45%+ growth, or

clearly maintaining the growth trajectory

I don’t like confused management.

I want sound, confident management — people who know what they are doing and are clear in their communication.

That’s why I listen to 2–3 management concalls, not just one:

Are they guiding clearly?

Are they delivering on what they guided?

Or are they just painting rosy pictures?

I also want to be honest here — management quality alone cannot prevent fraud.

Frauds are almost always detected after they happen, not before.

According to me, the only practical early warning signal is the pace of sales growth.

In my upcoming blogs, I’ll explain how tracking sales growth alone can help spot potential problems early.

I Buy the Future, Not the Past

I am a growth investor, not a value investor.

I never buy stocks that are down 40–45% from their highs, no matter how good the story sounds.

Why?

Because for a stock to double, it must cross its 52-week high anyway.

So I prefer to:

Buy near 52-week highs

Buy strength, not weakness

Buy stocks that are already being rewarded by the market

I always say this clearly:

I buy stocks high. I don’t buy stocks low.

PE Doesn’t Matter Much to Me, PEG Does

I don’t give much importance to PE.

PE alone is a useless metric if you don’t look at growth.

I focus on PEG (Price-to-Growth ratio), a concept popularised by Peter Lynch.

PEG = PE ÷ Growth rate

PEG < 1 → generally healthy

PEG ≈ 1 → acceptable for high-growth companies

That’s why I’m not a fan of low-PE stocks.

Low PE stocks usually stay low PE for a reason.

As William O’Neil said:

The biggest money is made in high-PE stocks.

Look at examples:

Trent looked expensive even at 150 PE, yet it delivered multi-bagger returns

PE never killed those stocks — growth slowdown did

If sales growth slows, no PE makes sense.

If sales growth is improving, almost any PE makes sense.

Recent examples:

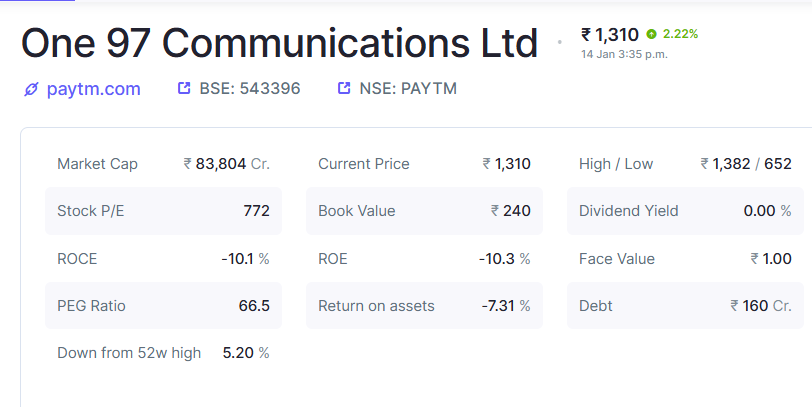

Nykaa

Paytm

Earlier they were growing at ~10%. Now growth has improved to ~25%.

Despite very high PEs, the stocks are near all-time highs — because the market rewards improvement, not valuation comfort.

What I Don’t Care About

I don’t focus on:

FII holdings

DII holdings

I honestly don’t care what FIIs or DIIs are doing.

They operate under:

Heavy regulations

Mandates

Portfolio constraints

You’ll never truly know why they are buying or selling.

I only focus on:

Growth

Management execution

My Risk & Execution Style

I use weekly charts for investing and positional trades

I look for patterns like VCP (Volatility Contraction Pattern)

I enter only when risk is clearly defined

Risk management is non-negotiable:

I don’t risk more than 8%, even for investments

If a stock goes 8% below my buy price, I exit — no emotions

And one more important thing:

I average up

I never average down

If I bought at 100, I’ll buy again at 120 — never at 80.

I’ll continue sharing more about how I invest, how I trade, and how I actually execute this framework in real markets.

Don’t worry if everything doesn’t make sense right now — I’ll break it down step by step in the upcoming blogs.

This is just the foundation.

The real learning will come as we go deeper in the next posts.