BlackBuck Limited: One of My Highest Conviction Stocks for 2026

So today, let’s start with one of my highest-conviction stocks — BlackBuck Limited, earlier known as Zinka Logistics Solutions.

In my previous blog, I talked about the current market environment and why I am neutral on the overall Indian equity market for 2026. I also shared that while I am not very bullish on the broader market, I am very bullish on commodities and select high-quality, high-growth companies that can still create good wealth even in a slow or range-bound market.

BLACKBUCK

BlackBuck was started in 2015.

At its core, BlackBuck is a digital platform for truck owners in India.

If I explain it in very simple words:

BlackBuck is like “Uber for trucks” — but much bigger and much deeper than just booking trucks.

First, Understand the Industry

India is a country that runs on trucks.

Almost everything we use — food, cement, clothes, fuel, electronics — is transported by trucks.

But the trucking industry in India is still very unorganised.

Most truck owners:

Own 1 to 5 trucks

Use cash for payments

Depend on middlemen

Don’t track their vehicles properly

Lose money due to fuel theft and inefficiencies

This is where BlackBuck comes in.

BlackBuck Is a Platform Business

Before going deeper, it’s important to understand one thing:

👉 BlackBuck is a platform business.

Just like:

Nykaa connects buyers and beauty brands

Paytm connects users, merchants, and payments

CarTrade connects buyers and sellers of vehicles

BlackBuck connects truck owners with digital services they need to run their business smoothly.

BlackBuck does not own trucks.

It builds a digital platform and earns money by helping truck owners operate better.

So What Exactly Does BlackBuck Do?

BlackBuck provides a single digital platform (app) where truck owners can manage almost everything related to their trucks.

Through BlackBuck, a truck owner can:

Pay tolls digitally on highways

Track where the truck is in real time (GPS tracking)

Monitor fuel usage and prevent fuel theft

Make fuel payments digitally

Find loads (goods) to transport

Get help with vehicle financing

Manage documents and compliance

Instead of using many different people, systems, and apps, a truck owner can do all this in one place.

BlackBuck becomes the daily working app for a truck owner.

How Does BlackBuck Make Money?

BlackBuck makes money by:

Charging fees on digital toll payments

Earning revenue from vehicle tracking subscriptions

Making money from fuel payments and fuel sensors

Earning commissions from load matching and financing services

As more truck owners use more services on the platform,

BlackBuck’s revenue keeps increasing.

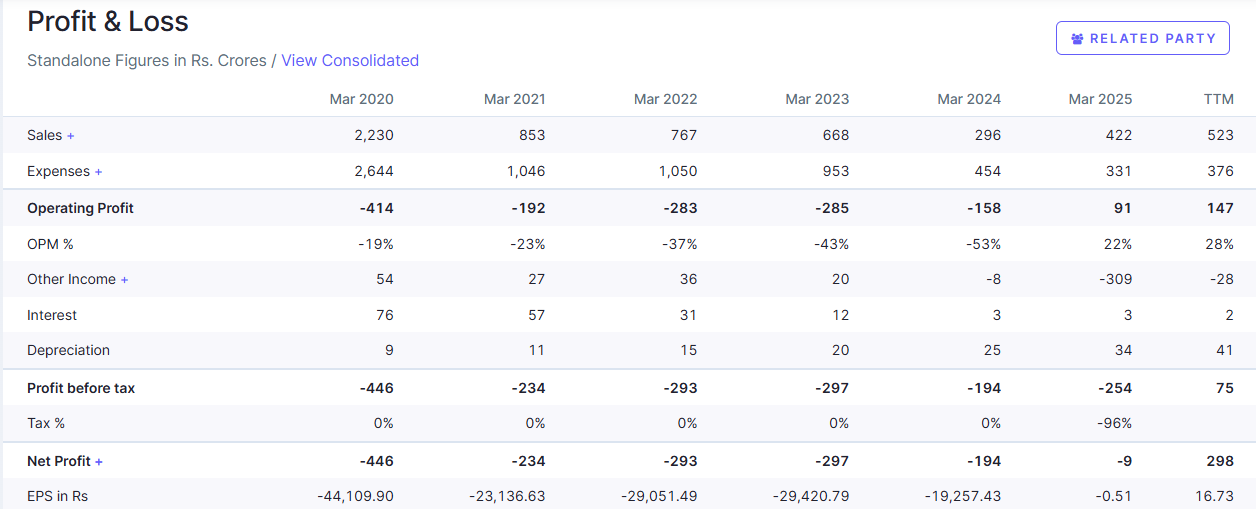

BlackBuck’s Financial Turnaround: Where the Real Story Begins

Now let’s talk about numbers,

For the last few years, BlackBuck was struggling financially.

The company was growing, but it was not profitable.

It was reporting losses (negative profits) and was still trying to find the right balance between growth and sustainability.

This is very common for platform businesses in their early years.

The Struggle Phase (Before the Turnaround)

For almost three years, BlackBuck:

Was making losses

Was investing heavily in building the platform

Was expanding users and services

Was not yet focused on profits

In FY24, the company reported a loss of around ₹194 crore.

At this stage, many investors lose patience.

But this is also the stage where the foundation is being built.

The Big Pivot Came in FY25

The real change happened in FY25.

This is the year when BlackBuck clearly showed that:

“We are no longer here just to survive — we want to scale and become profitable.”

In FY25:

Revenue grew by around 42–50%

Total revenue reached ₹422 crore

Losses reduced sharply to just ₹9 crore

Compared to a ₹194 crore loss in FY24

This massive reduction in losses tells us one thing very clearly:

👉 The business model started working.

This was the pivot point.

Strong Momentum From FY26 (The Real Turnaround)

After FY25, things started moving very fast.

June 2025 (Q1 FY26)

In the June quarter:

Revenue grew by 50–55%

The company reported ₹35 crore profit (PAT)

Compared to ₹28 crore profit in June 2024

This showed that profitability was not a one-time event.

September Quarter (Q2 FY26) – The Proof Quarter

This quarter truly confirmed the turnaround.

In Q2 FY26:

Revenue was ₹149–167 crore (around 50–60% growth)

Profit after tax (PAT) was ₹29–31 crore

In Q2 FY24, the company had a loss of ₹270 crore

This is not just improvement —

👉 this is a complete business turnaround.

You simply cannot compare these two periods.

What Is Driving This Growth?

The most interesting part is where the growth is coming from.

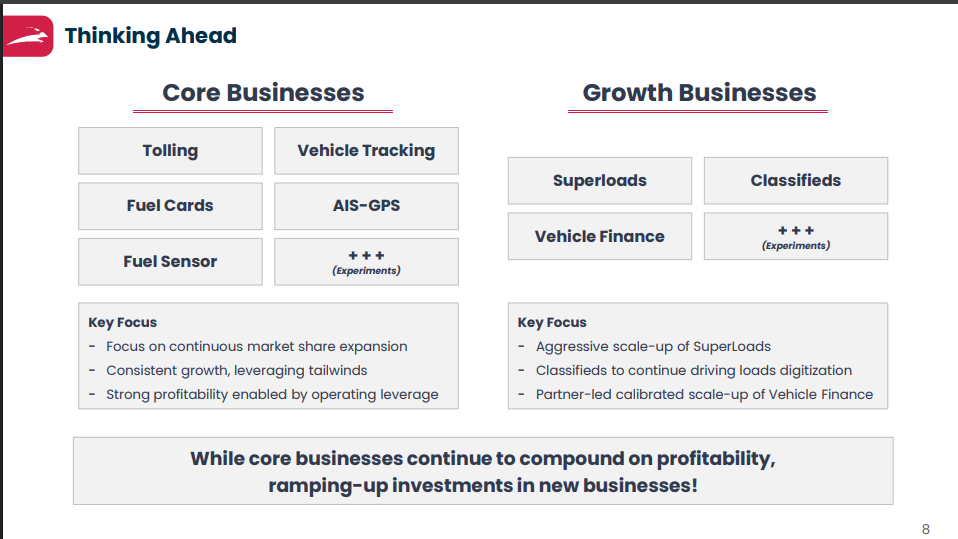

1. Core Business Is Still Strong

Core businesses (toll payments, vehicle tracking, fuel services)

Growing at 36% year-on-year

Stable, recurring, and profitable

This gives the company a solid base.

2. Growth Businesses Are Exploding

This is where things get exciting.

BlackBuck’s growth businesses (especially SuperLoads) grew by:

230% year-on-year

That is a huge number.

SuperLoads is scaling very fast and:

Helping truck owners find loads more efficiently

Increasing platform usage

Adding high-growth revenue streams

Because of this:

Overall company revenue is growing at ~50–60%

The business is becoming more diversified

The future growth runway is expanding

Why I Decided to Go Deeper Into BlackBuck

All these things I discussed earlier were the main triggers that pushed me to study BlackBuck more deeply.

When a company:

Shows strong revenue growth

Turns from losses to profits

And does this consistently

…it deserves a closer look.

So I started digging deeper into BlackBuck’s numbers, history, and management commentary.

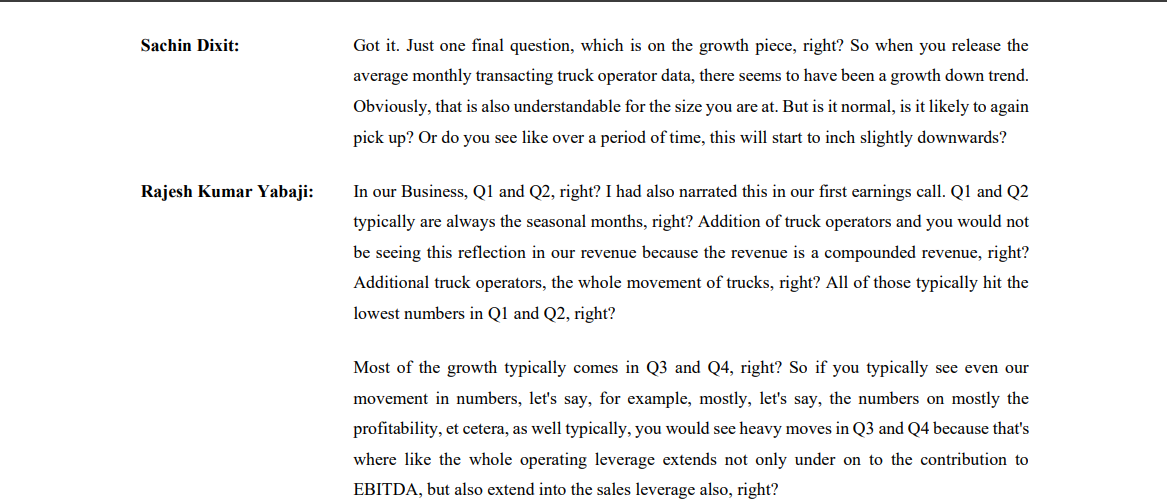

One Important Pattern in BlackBuck’s Business

If we look at BlackBuck’s history, one pattern is very clear:

👉 H2 (second half of the year) has always been stronger than H1.

This means:

Q3 and Q4 are usually better than Q1 and Q2

Growth accelerates in the second half

Profits also improve in H2

This is mainly because:

Trucking activity improves in the festive and year-end period

Demand for logistics increases

Operating leverage kicks in

So the best numbers are still ahead, not behind us.

Management Is Also Confident About H2 FY26

This is not just my assumption.

The management themselves have clearly said that:

They are very bullish on Q3

They expect strong performance in Q3 and Q4 of FY26

This gives additional confidence that:

The momentum we are seeing is not temporary

The business is entering a strong growth phase

Revenue Estimate for FY26

BlackBuck has already delivered strong numbers in H1 FY26.

If growth continues as expected, I can see:

FY26 revenue in the range of ₹630–650 crore

That is roughly 50% year-on-year growth

For a company that has just turned profitable,

this kind of growth is very powerful.

Profit (PAT) Estimate for FY26

Even if we take a conservative approach:

Let’s assume:

H2 FY26 only matches H1 FY26

No major upside surprise

Even then:

FY26 PAT can reach ₹132–135 crore

This is a big change for a company that was:

Making losses just a year ago

What Does This Mean for Valuation?

If BlackBuck earns around ₹135 crore profit in FY26,

then at current prices:

Forward P/E comes to around 86

PEG (P/E compared to growth) comes to around 1.7

Now let’s compare this with other platform businesses.

How Platform Companies Are Valued in the Market

Platform businesses usually trade at very high valuations, because:

They are scalable

They have high growth

They have strong customer stickiness

For example:

Paytm has traded at very high 1000 P/E levels

Zomato has traded at extremely high 1500 P/E levels

Nykaa has also traded at very high valuations and 700 P/E

CarTrade trades around 70 P/E

So compared to these:

BlackBuck at 80–90 P/E with 50% growth

Looks reasonable, not expensive

One Important Rule of Investing

A high P/E is not a problem.

👉 A high P/E becomes a problem only when growth is missing.

In BlackBuck’s case:

Growth is strong

Profits are real

Platform business model is working

That’s why, in my opinion:

A 130–150 P/E is possible if growth sustains

And platform businesses do deserve premium valuations

My Intrinsic Value on BlackBuck

Based on all this analysis —

the turnaround, strong growth, improving profitability, platform business model, and management confidence — I tried to arrive at a rough intrinsic value for BlackBuck.

Again, I want to clearly say:

This is my personal estimate, not a guarantee or a recommendation.

If BlackBuck:

Delivers ₹630–650 crore revenue in FY26

Generates ₹132–135 crore PAT

Sustains ~50% growth

And the market continues to value platform businesses at premium multiples

Then, in my view, the intrinsic value of the stock can lie somewhere in the range of ₹1,000 to ₹1,200 per share.

A Small Note on the Promoter & Leadership

One of the biggest reasons I am confident about BlackBuck is its promoter and leadership.

The company is led by Rajesh Yabaji, the founder and CEO of BlackBuck Limited.

Rajesh Yabaji is highly educated and has a strong academic background:

Engineering graduate from IIT Kharagpur

MBA from IIM Bangalore

But more than degrees, what matters to me is execution and patience.

He has been building BlackBuck for nearly 8–10 years, starting from 2015.

For many years, the company was loss-making, faced challenges, and required continuous investment. Despite this, the promoter did not give up, did not chase shortcuts, and stayed focused on building a strong platform.

Over the years:

He deeply understood the trucking ecosystem

Built products ground-up for Indian truck owners

Invested heavily in distribution and trust

Slowly turned the business from losses to profits

Today, when BlackBuck is finally showing strong growth and profitability, it clearly reflects years of hard work and long-term thinking.

I personally like promoters who:

Stay with the company through tough phases

Focus on business first, stock price later

Play the long game.

Technical View

Technically, BlackBuck Limited looks strong. The stock is in a smooth uptrend on the weekly chart and is holding above its 10-week EMA. Even in a weak market, it is only about 15% below its all-time high, showing strong relative strength. After a breakout in August 2025, the stock is forming a healthy base. If upcoming results are strong, a fresh upward move may start. Overall, momentum remains positive, though markets should always be watched closely.

Final Thoughts & Risk Management

Wrapping up my analysis on BlackBuck Limited, as of now, I remain very bullish on the stock.

However, one important thing I strongly believe in is this:

The best investor or trader is not the one who is always right, but the one who changes his view quickly when he realises he is wrong.

As of today, BlackBuck looks like a solid bet — strong growth, improving profitability, and clear operating leverage. As long as the company continues to:

Grow at a healthy pace

Improve profits faster than sales

Execute well in Q3 and Q4

…the story remains intact.

But markets do not reward blind belief.

If:

Growth slows down

Operating leverage disappears

Or results disappoint in Q3 or Q4

Then we should be quick to exit, without emotions.

Being attached to a stock or believing only in a story never works in the market.

Right now, BlackBuck is one of my best ideas, and if the overall environment remains supportive, I do see the stock making new all-time highs over time.

Disclaimer

This content is shared purely for educational purposes and reflects my personal views.

Please consult your financial advisor before making any investment decisions.